Following my recent post about Fresenius. I went deeper into their financials trying to understand why the share price dropped over the last years. In 2017 they acquired a Spanish hospital group (Grupo Hospitalario Quirónsalud) which increased Fresenius’s debt by a lot. The share price decline started since. Margins are declining since too. Then they had another larger acquisition attempt in 2018 which they terminated last minute – thankfully. It seemed to be a bold decision at the time. The CEO was heavily criticized for wasting time and money on the acquisition and then pulling out last minute. I think this shows that he has a flexible mind, is willing to admit mistakes and moves on (a good ability). Later it turned out that the target (Akorn) inflated their financials and their share price collapsed after Fresenius terminated the takeover attempt. The market is now concerned about their growth by acquisitions strategy as it seems they didn’t add much quality since 2017. Margins, ROE and ROIC are declining. Following their acquisitions debt and goodwill were increasing. They started only last year with some small goodwill impairments.

Other successful holding companies which are growing with acquisitions like Danaher have also large and increasing goodwill on their balance sheet and it doesn’t stop the market pushing their share prices higher. I believe if Fresenius proves that they can create shareholder value when acquiring other companies then trust will return and the share price should rebound nicely.

Another concern is probably market risk as some of the acquisitions were in Spain (Quirónsalud + Eugin Group). Spain is seen as one of the structural weaker economies in Europe adding additional uncertainty. Uncertainty is not well liked by the market.

The later acquisition of Eugin group from NMC Health (which went into administration – triggered by COVID) adds some additional uncertainty given their recently not so successful takeovers. However, I think if this gets approved Fresenius got a good deal by scooping a growing business from a company running into financial difficulties. The acquisition will cost an expected EV/EBITDA 11.4 which is not bad under current market condition for a business in a defensive industry and growing yearly by 10%. It would make Fresenius Helios become the leading international fertility provider.

Valuation estimations on various models:

- EV/EBITDA valuation: € 55/share – on historical measures and fair value in comparation to peers.

- Gurufocus Fair Value: €57.04/Share

- Implied equity value: at zero growth in 2021 (more likely higher) and thereafter 5% annual CF growth and WACC 6.5% until 2025. Terminal growth rate 2%: € 69.15.

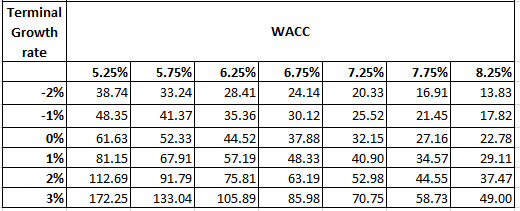

See below matrix for different WACC and terminal growth rate assumptions:

Today’s share price assumes no terminal growth for the business. This is very unrealistic given the companies acquisition strategy and international expansion, the secular trend of an aging society focusing on better healthcare and an increasing inflation. The company announced that the business is meaningfully impacted by the pandemic. This is only temporary as the pandemic will pass on due to increasing vaccination rates and development of treatment methods. I think Fresenius SE offers a good margin of safety at today’s share price with a discount of 41% to my estimated implied equity value. Recently I used the opportunity to purchase shares of this European dividend aristocrat.

- Fresenius SE ISIN: DE0005785604

- Share price 30.04.2021: € 40.86

Disclosure: I’m long Fresenius SE. No investment advise. Please do your own research.

Interesting read. Fresenius has caught my eyes recently. There is a lot to like about that German dividend aristocrat, such as the relative defensive business model and a secular trend that should support organic growth in the long run.

I am not sure though that Fresenius Management has had good acquisition strategies. LVMH, Nestlé, Danaher, L‘Oreal etc. have been a whole lot better in communicating, preparing and integrating of acquisition targets. It has been a debacle, how Fresenius executes its acquisition strategies.

But you are right, the stock price has been punished more than enough and there is great recovery potential.

Cheers

MyFinancialShape

Thanks for your comment! LVMH and Danaher are excellent capital allocators. Nestle and L’Oreal are also great(Btw. Nestle is run now by former Fresenius CEO). Pity they look always expensive for me-I should probably start a savings plan and just let it run.

I think Fresenius had only one „debacle“ with Akorn but in my point of view they dealt with it quite good. It just takes time to proof it to the market. It could have also ended like Bayer‘s Monsanto acquisition or Altria‘s Juul investment.